Health Spending Accounts For Canadians Explained

A Health Spending Account (HSA), also known as a Health Care Spending Account (HCSA) or Health...

By

October 19, 2021

By

August 12, 2020

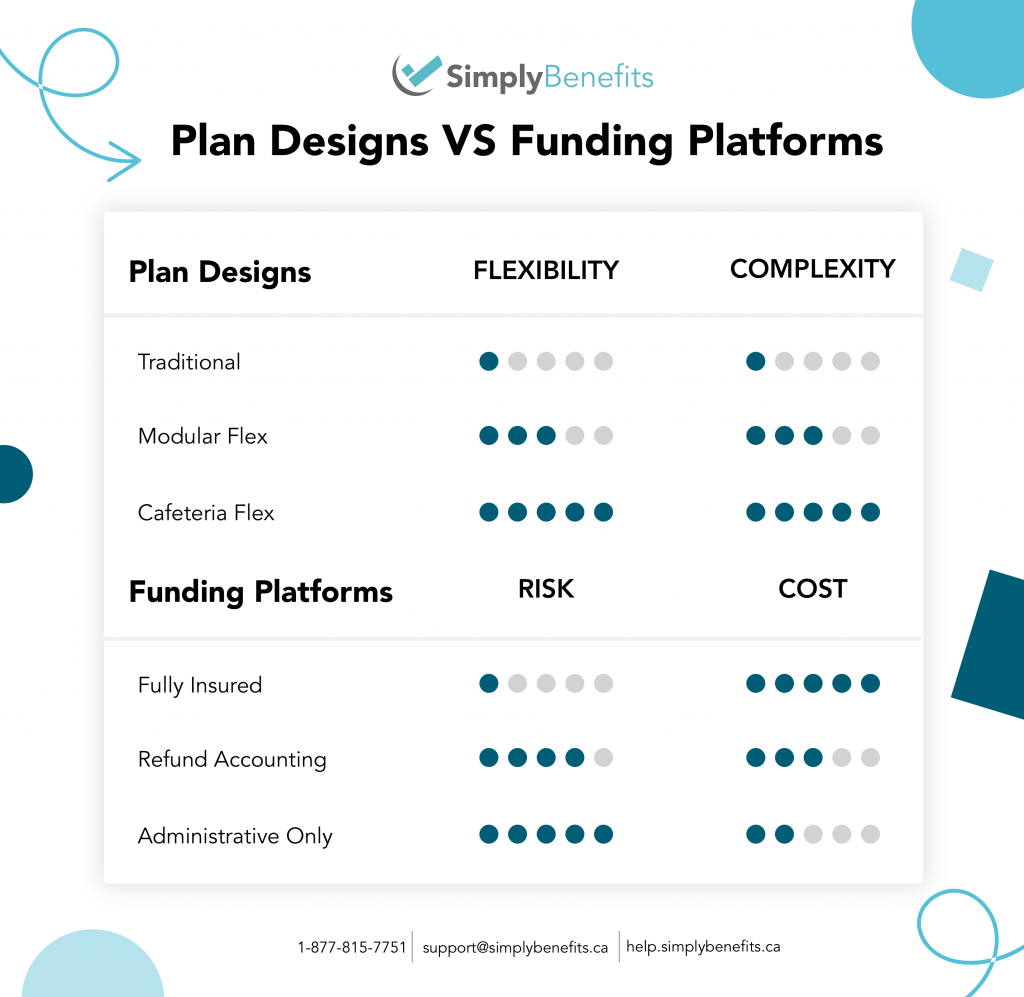

There’s a lot that goes into designing and creating an Employee Benefits plan. From coverage levels to spending accounts, there are many different options to pick from. In the insurance world, we call these options Plan Designs and Funding Platforms and deciding which ones to use are among the first steps to designing an employee benefits plan. If you don’t know what those things are, don’t worry. In this blog, we’ll describe the different kinds of plan designs and funding platforms that Simply Benefits offers so you can decide which fits your company the best.

Plan Designs

The first step of a group benefits plan is the plan design itself. A plan design is the outline of everything that will be included in a benefits package. From health insurance to long term disability, they outline all of the nitty-gritty details. Designing a plan is not a simple task, but you typically do it alongside an insurance broker or insurance advisor who will manage creating and pricing the details. Simply Benefits offers three common types of plan designs: traditional, modular flex, and cafeteria flex.

1. Traditional

This type of plan design gets its name from being the simplest and most commonly used plan design, with 72% of employees having a traditional plan in 2020. In this case, the employer picks and chooses the benefits that they want to include in the benefits plan. This benefits plan is then applied to all employees without any variation between employees, or any choice.

Here’s an example. Let’s say an employer wants a plan that provides 80% coverage for dental, vision, paramedical, and prescription drugs. Each employee will receive the same coverage without any variation depending on their class. This means that employers can have a “Traditional” plan design with their desired classes, and each class offers different coverage amounts but employees do not have a say in which class they are in, or what benefits are included in their plan.

Note: Classes are created within a plan design to offer different coverage levels for certain employees (ex. C-Suite, Management, Employees, etc).

Pros & Cons

This plan design is less popular these days because it’s lacking in flexibility. Employees aren’t as excited about mandatory pre-designed plans, and 67% of them reported that they would prefer a flex plan. However, this style of benefits is easy to administer and keep track of, since all plans are the same, and monthly premiums remain consistent (employer pays the same amount for health benefits each month). This style of plan is great for smaller businesses that don’t have as much administrative power or time, but still want to provide benefits to their employees.

2. Modular Flex

This plan design has slightly more flexibility. With modular flex, employees can select between plans with different tiers of benefits (usually 3). Each plan will have different levels or amounts of coverage that are typically aimed at a specific demographic, like singles, families, or older individuals. Traditional health benefits like drugs, paramedical services, dental, and vision are offered and the employee can select the level of coverage based on the plan levels.

Here’s an example. Let’s say an employer at a company creates three different plans with different levels of coverage for health benefits. One plan offers basic level of coverage and it is labelled “Bronze”, one offers more coverage compared to the bronze level and it is labelled “Silver”, and the most comprehensive in coverage is labelled “Gold”. An employee working at this company who is single and has no dependents will likely choose the basic option (Bronze) because they don’t need the extra coverage, and then they would receive more towards their Health Spending Account (HSA). A newly married employee however may want more coverage for themselves and their spouse, so they would select “Silver” and have a small remaining HSA amount. An older employee with a family may choose the Gold plan with the highest level of coverage, and then have no HSA.

Pros & Cons

As much as modular flex plans are flexible, they fall short in some areas. After employees choose their plan, they usually can’t change it until the next year. Modular flex is also slightly more complicated to administer than traditional plans. However, if you can overlook that, modular flex can be a great option because of its flexibility and attractiveness to employees. This is a good option for employers that have administrative abilities that also want to offer flexibility.

3. Cafeteria Flex

This type of plan design offers the most flexibility. With cafeteria plans, employees receive a dollar amount and get to select which benefits they’d like to include in their own personalized plan. Employees can select the benefits and the level of coverage with their flex credits. Once the credits are all used up, employees can either purchase additional coverage or pay out of pocket.

Here’s an example. Let’s say an employee is given a $2000 dollar amount in flex credits. This employee decides to allocate their flex credits towards the basic dental, drug, and vision coverage which uses up all of their flex credits. If this employee also wants paramedical coverage, they have to purchase that coverage themselves.

Pros & Cons

This type of plan is the most difficult to administer because of the customized employee plans. However, cafeteria flex provides employees with the most flexibility and can work with organizations of all sizes. On top of that, if employees get to choose their own benefits, they’re more likely to get use out of them. Cafeteria flex plans are a good option for employers who want to give their employees flexibility. These plans also work well for small businesses that want to provide benefits to their employees in a cost-effective way.

Funding Platforms

Funding platforms are the method that the employee benefits plans are administered. This is essentially how the benefits will be paid for and how the insurance will be provided. With this, there are a couple of options for how much risk a company will take on, and how much a company will pay for certain benefits. Simply Benefits offers three types of funding platforms: fully insured, refund accounting, and administrative services only.

1. Fully Insured

Fully insured is probably the easiest platform to understand and administer. With this funding platform, the insurer takes on all the risk and the employer pays a set monthly premium per employee no matter how much is used. The monthly premium comes from how much the benefits plan typically costs to administer. The average usage of the benefits that employers want to target is about 80% of the total premium, meaning for every $1 they pay in premium, they want their employees to use $0.80 on health services.

Here’s an example. A company pays a monthly premium of $5,000 every month no matter how much or how little their employees use their benefits. If one of this company’s employees gets sick and has large medical bills, they are protected and usually don’t have to pay more than their premium. This means that even if their employees spend $300, or $10,000 each month on health benefits, employers will still always pay $5,000 a month in premium. Based on annual usage, the employer’s monthly premiums will increase or decrease the following year.

Premium: The monthly amount (cost) that insurers charge for a chosen group benefits plan.

Pros & Cons

Fully insured is the most expensive platform type because you’re paying the same amount per month no matter the amount of benefits that are used. However, the biggest advantage of these platforms is that it’s the least risky because you don’t pay an overuse fee. Fully insured is a good option for small to medium-sized companies, because of the low-risk factor, or new companies that aren’t yet sure how much benefits their employees will be using.

2. Refund Accounting

With refund accounting, the employer is responsible for estimating the number of claims that will be used throughout the year. This can be done by looking at demographics and trends, or just having a good understanding of the amount of benefits that employees will use. Normally, this is a good option for businesses that have been using employee benefits for a few years. The employer then pays a set monthly price based on their estimate. At the end of each year, the final bill is calculated based on if that organization went over or under their monthly premium, and employers have to pay the variance.

Here is an example. A company sets its monthly premium at $5,000. By the end of that calendar year, the company ended up paying $500 more dollars every month. Because the company went over their monthly premium, they are going to have to pay a deficit through a premium increase. If the company was under target, they would receive a reimbursement amount.

Pros & Cons

If you underestimate how much benefits your employees use, you have to pay. This makes refund accounting slightly riskier than fully insured. However, if your estimate is good then this ends up being very cost-effective because you only pay for what you actually use. This is a good option for employers that have been in the benefits space for a long time and understand and know their employees benefit spending habits very well.

3. Administrative Services Only

Also known as ASO, this plan centers around the fact that the employer is responsible for funding claim costs. A third party (like Simply Benefits) is chosen to administer the plan and charges fees for its services. This is typically in the form of monthly payments for claims adjudication. The company pays an administration fee for each claim that is submitted.

Here is an example. At a company, they pay for each claim submitted by the employee in full. Meaning that for every claim submitted, the employer is responsible for paying for the entire bill. They are also charged a small administrative fee for paying the claim, storing, etc. If their employees submit a total of $500 in claims in March, then the employer would only pay $500 plus the administrative fees. If their employees submit a total of $2,000 in claims in April, then the employer will pay the $2,000 plus the administrative fees.

Pros and Cons

Since ASO plans are based on actual paid claims rather than anticipated claims, employers are responsible for paying if the actual claims exceed the budget. This means that ASOs are the riskiest platform as the insurer itself doesn’t take on any risk. However, ASOs can offer employers greater control over their benefits plan design and how much is purchased through the plan. This platform would work best for companies that are comfortable with taking on the risk and understand their employee’s benefits and spending habits.

Final Thoughts

Behind every good employee benefits plan, there is a plan design and funding platform. There are pros and cons to each type of these, but a common trend is that flex plans are becoming more popular among employees. Below is a summary chart that you can reference when you are creating your employee benefits plan.

Hopefully this guide helped you understand which one would fit your company best. If you have more any questions, reach out to one of us at support@simplybenefits.ca.

Disclaimer: Please note that the information provided, while authoritative, is not guaranteed for accuracy and legality. If you are a Simply Benefits plan member, you can look up more information on your specific plan coverage under the “Plan Coverage” section on your account, or speak to your administrator for more information.

References

Sanofi-aventis Canada Inc. “The Sanofi Canada Healthcare Survey; Future Forward Frontline Perspectives on the Future of Health Benefit”, June 24, 2020. https://www.sanofi.ca/-/media/Project/One-Sanofi-Web/Websites/North-America/Sanofi-CA/Home/en/Products-and-Resources/sanofi-canada-health-survey/sanofi-canada-healthcare-survey-2020-EN.pdf

Terms + Conditions

Simply Benefits Inc. (“us”, “we”, or “Simply Benefits”) is committed to privacy and the protection of your information. By using Simply Benefits’s website, mobile and other applications, and related Services made available through the Apple App Store, the Google PLAY Store, or otherwise on the Internet (together, the “Simply Benefits Applications” or “Applications”), you acknowledge that you accept the practices and policies outlined in this Privacy Policy (“Privacy Policy“). Unless otherwise defined herein, capitalized terms shall have the meanings assigned to such terms set forth in the Terms of Service and which incorporate this Privacy Policy by reference.

Privacy Policy

In accordance with Canada's *Personal Information Protection & Electronic Documents Act* ("PIPEDA") we have established policies on how we collect, use and protect any information that you give us when you use our website or services.

Required Regulatory Information

Simply Benefits collects information needed to provide services and meet the regulatory requirements of our industry. When you open an account or sign up for services, we collect personal information which may include but is not limited to the following:

Your name and date of birth

Contact details

Nature of your employment or business

Details about your dependents

Demographics

Other information relevant to the services we provide

We may receive passively-collected information through a variety of methods, including “cookies” to collect information.

Cookies are text files containing small amounts of information which are downloaded to your device when you visit a website. Cookies are then sent back to the originating website on each subsequent visit, or to another website that recognizes that cookie. You can get more information about cookies here.

Simply Benefits uses cookies to track and measure site performance and gather analytics on usage. This information is anonymous and is only used by Simply Benefits to measure and improve our site.

When sending e-mail we may use tracking pixels and urls to help us measure open rates for e-mails and link clicks. This tracking information is used internally only to help us provide relevant content and is never shared with any third parties.

If you choose, you may set your browser to notify you when you receive a cookie, giving you the chance to decide whether or not to accept it.

We use analytics tools and other third party technologies, such as Google Analytics, to collect non-personal information in the form of various usage and user metrics when you use our online Sites and/or Services.

We also use online advertising to reach new potential clients and remarketing tools that allow us to target ads to specific groups of people who have previously interacted with WealthBar’s websites.

Google allows individuals to opt out of it’s advertising cookies from its ad settings page.

Google has additional information available about their Remarketing Privacy Guidelines, and Restrictions.

Simply Benefits may use third parties to store and process data. Simply Benefits will ensure that such third party service providers have significant expertise with data and digital privacy. Simply Benefits will ensure that personal data is stored and transmitted in encrypted format using technology such as SSL. Third party data storage and processing providers may be located in the United States and as a result personal information may be subject to U.S. privacy law which may differ from Canadian privacy law.

The information we collect is used so we can communicate with you, provide benefits and insurance management services, improve our products and services, and meet our regulatory obligations.

We share only the information which is reasonably required in the normal course of business with third parties such as our custodians, securities regulators, auditors, legal counsel, or law enforcement agencies, to enable them to fulfill their obligations to Simply Benefits and our clients. We may also disclose your personal information to third-party service providers, affiliates and agents in order to assist us in providing the services you requested and to fulfil the purposes for which your personal information has been collected. Outside of this we shall not sell, distribute or lease your personal information to third parties unless we have your permission or are required by law to do so.

We are committed to ensuring that your information is secure. In order to prevent unauthorized access or disclosure, we have put in place suitable physical, electronic and managerial procedures to safeguard and secure the information we collect online. In the event that we share your personal information with third-party service providers, affiliates and agents, these parties will be required to adhere to strict confidentiality obligations and practices.

If you have a question, concern or complaint about our privacy policy, please send your comments and your contact details to our Privacy Officer in writing to the following address:

Simply Benefits Corp.

601-460 Doyle Ave,

Kelowna BC

V1Y 0C2

product@simplybenefits.ca

If you believe that any information we have on file for you is incorrect or incomplete, please write to or email us as soon as possible, at the above address. We will promptly correct any information found to be incorrect.